Liutauras Ulevičius, President of the National Gambling and Gaming Business Association (NGGBA), presented financial data and shared his insights on the development of the gambling industry in the Baltic countries during the post-COVID period.

NGGBA is a Lithuania-based think tank operating within the Baltic region.

Three markets via the GGR perspective

Gross gaming revenue (GGR) is a standard market figure. It is easy to calculate and use it for comparison purposes. It is the main parameter that describes the market size, market shares, and market structure. Nevertheless, national regulators are reluctant to publish these basic periodic figures, and it takes time for operators to collect trustworthy data.

NGGBA has been operating for 30+ years in the Baltic region and collects major market characteristics from official (national regulators), semi-official (corporate and analyst data), and even indirect/unofficial sources. Therefore, these are GGR figures (in mln. €) for the Baltic states in 2019-2024:

| Estonia | Latvia* | Lithuania | |

| 2019 | – | 307,1 | 162,5 |

| 2020 (~3/4 Covid) | ~105 | 159,6 | 150,4 |

| 2021 (~1/4 Covid) | – | 128,0 | 193,6 |

| 2022 | ~336 (iGaming) | 264,8 | 252,2 |

| 2023 | – | 288,6 | 288,5 |

| 2024 | ~385 | 299,4 | 310,7 |

| 2025 H1 | – | 66,4** | 167,6 |

*Figures above include all gambling services (including lotteries according to EU definitions). Latvian data do not include GGR from lotteries. Estonian data is sporadic.

Responsible gambling – from empty declaration to gambling closures?

Self-exclusion schemes (thousands of registered self-excluded persons on December 31st) and number of requests (total/active):

| Estonia | Latvia | Lithuania | |

| Total population (as Jan 2025) | 1 370 | 1 857 | 2 830 |

| 2019 | – | – | 11,5 / – |

| 2020 (Covid) | ~14 | – | 17,3 / – |

| 2021 (Covid) | – | 24,6 / 17,2 | 24,8 / – |

| 2022 | – | 40,6 / 14,8 | 36,2 / 12,7 |

| 2023 | – | 58,0 / 31,7 | 50,1 / 15,3 |

| 2024 | – | 76,2 / 35,8 | 66,5 / 18,1 |

| 2025 H1 | ~19 | – | 78,7 / 19,9 |

*Data is taken close to the end of the calendar year.

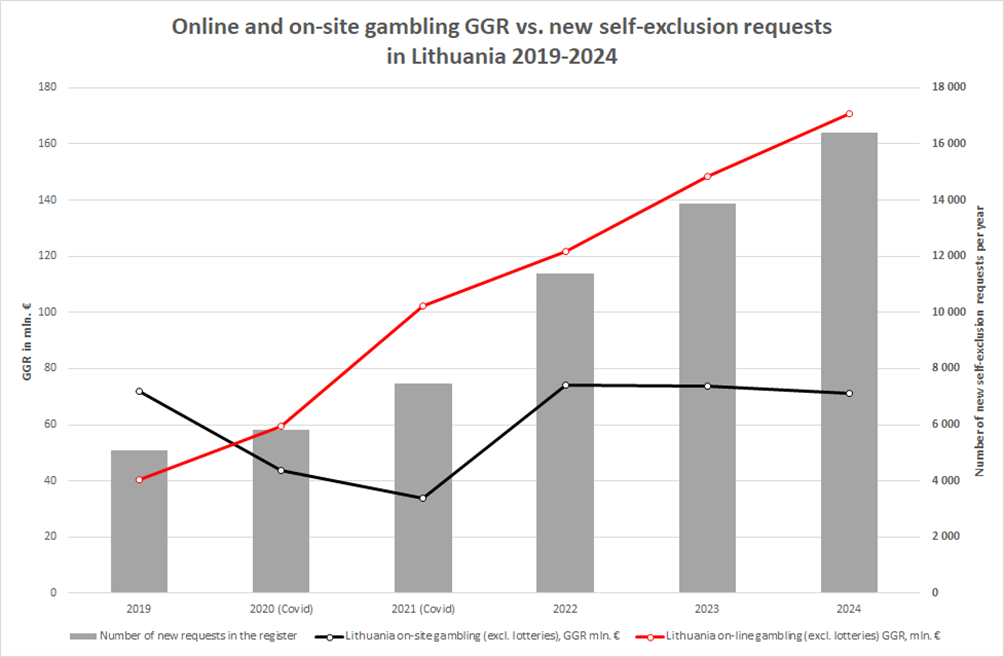

While detailed Estonian figures are not disclosed, Latvian and Lithuanian examples are very straightforward, and a clear correlation between online growth vs. the number of self-exclusion requests is evident. For example, Lithuanian data is divided into on-site, online, and stream of requests:

Correlation between online growth and self-exclusion participants

| Lithuania on-site gambling (excl. lotteries), GGR mln. € | Lithuania online gambling (excl. lotteries) GGR, mln. € | Number of new requests in the register | |

| 2019 | 72,1 | 40,5 | 5 079 |

| 2020 (Covid) | 43,9 | 59,6 | 5 816 |

| 2021 (Covid) | 34,0 | 102,2 | 7 485 |

| 2022 | 74,1 | 121,7 | 11 388 |

| 2023 | 73,8 | 148,4 | 13 876 |

| 2024 | 71,2 | 170,6 | 16 407 |

| 2025 H1 | 35,4 | 96,0 | *13 690 |

It becomes too evident when presented in a graph. While the on-site gambling GGR has stalled (remains at the 2015-2016 level), the flow of requests is directly linked to the online GGR growth tempo:

The hidden truth? Irresponsible gambling online

While Latvia and Estonia have no limited gambling services, Lithuania has services divided into A and B segments (unlimited and limited). When gamblers are allowed to choose the service, they jump to the most risky unlimited services.

For example, the Lithuanian market GGR shares between unlimited and limited gambling services in 2015 (the last year before online legalization) and 2024:

| Gambling services | 2015 | 2024 |

| Unlimited bets (casino tables, casino A EGM, betting) | 44,4% (53,4 mln. €) | 67,2% (208,9 mln. €) |

| Limited bets (B EGM, bingo, toto, lotteries) | 55,6% (66,7 mln. €) | 32,8% (101,8 mln. €) |

Most interesting is the online environment, where all services are available for consumers and respective market shares:

| Online gambling service | Online market share in 2024 |

| Online casino tables | 8,7% (14,9 mln. €) |

| Online A EGM | 66,8% (113,9 mln. €) |

| Online B EGM | 2,0% (3,3 mln. €) |

| Online betting | 22,6% (38,5 mln. €) |

| Online bingo | No providers |

| Online toto | No providers |

| Online lotteries | No data are provided, expert estimates ~5-10% from total lotteries GGR (~7-15 mln. €) |

The gamblers’ choice is clear – if allowed, they choose the most risky and dangerous services. While the safe and responsible services receive only 2% market share.

Best practice? Look at Germany and the United Kingdom

In the ideal scenario, gambling service providers should aim at responsible gambling, but in a competitive market, the force to earn maximum profit rules. Therefore, state policy is a key to a long-term, sustainable gambling market.

Examples?

Germany, interstate treaty 2021 (Glücksspielstaatsvertrag 2021):

– Maximum online bet limit = 1€

– Monthly deposit limit (per all operators) = 1,000€

The United Kingdom (from May 2025):

– Maximum online bet limit (up to 24 years) = 2£

– Maximum online bet limit (25+ years) = 5£

Alternative “best practices”? Look at India, look at Russia, and other “closed” markets:

• Several years of “sky-rocket” market;

• Huge social problems and political hunt / blame-shifting;

• Market closure or nationalization.

Don’t forget to subscribe to our Telegram channel!